#256: VC Midyear Update (2025): Liquidity, AI, & Secondaries

Insights from PitchBook's US Venture Capital Midyear Update

At the midpoint of 2025, the U.S. venture capital market is sending mixed signals—renewed activity in AI and secondaries, but persistent headwinds in liquidity and fundraising. PitchBook’s US Venture Capital Midyear Update frames the landscape clearly: this is a market in transition, not recovery.

Liquidity Outlook: Window Still Narrow

Early 2025 opened with optimism: strong public markets, early IPOs, and momentum in late-stage financing. But macro factors—tariff rollouts, geopolitical friction—have weighed on sentiment. PitchBook now sees a slower recovery path:

“A return to a normal liquidity environment in 2025 now appears unlikely.”

A handful of IPOs have broken through—eight venture-backed U.S. companies debuted above $1B valuations, including CoreWeave—but PitchBook notes:

“While the number of listings may not meet initial expectations, a few companies have managed to navigate the volatility successfully.”

Selective success hasn’t translated into broad-based confidence. Most mature companies remain private, and exit markets remain constrained.

Late-Stage Capital Remains Bottlenecked

Deal activity has held steady in Q1 and Q2, but capital availability is still skewed. PitchBook highlights that:

“The demand-supply imbalance for late- and venture-growth-stage companies will remain above the 2016–2020 trend averages.”

Investors are narrowing focus. According to the report:

“Capital [is] flowing into select later-stage companies,” primarily those with AI tailwinds, while “exit activity continues to lag, keeping many of those mature companies still private and limiting downstream liquidity for LPs.”

The implication? More capital locked in, and slower pacing across vintages. That pressure compounds for LPs seeking distributions.

AI Still Leads the Cycle

If there’s one clear outlier, it’s AI. PitchBook finds that:

“Valuation growth for AI startups significantly outpaces non-AI companies at most stages.”

Series A AI companies are experiencing nearly 50% annualized valuation growth—levels that approach the peaks of 2021–2022.

Still, optimism has its limits.

“VC remains in a challenging market with less capital available to support the hyper-growth rates seen in previous years,” PitchBook cautions.

Even in AI, expectations are being recalibrated.

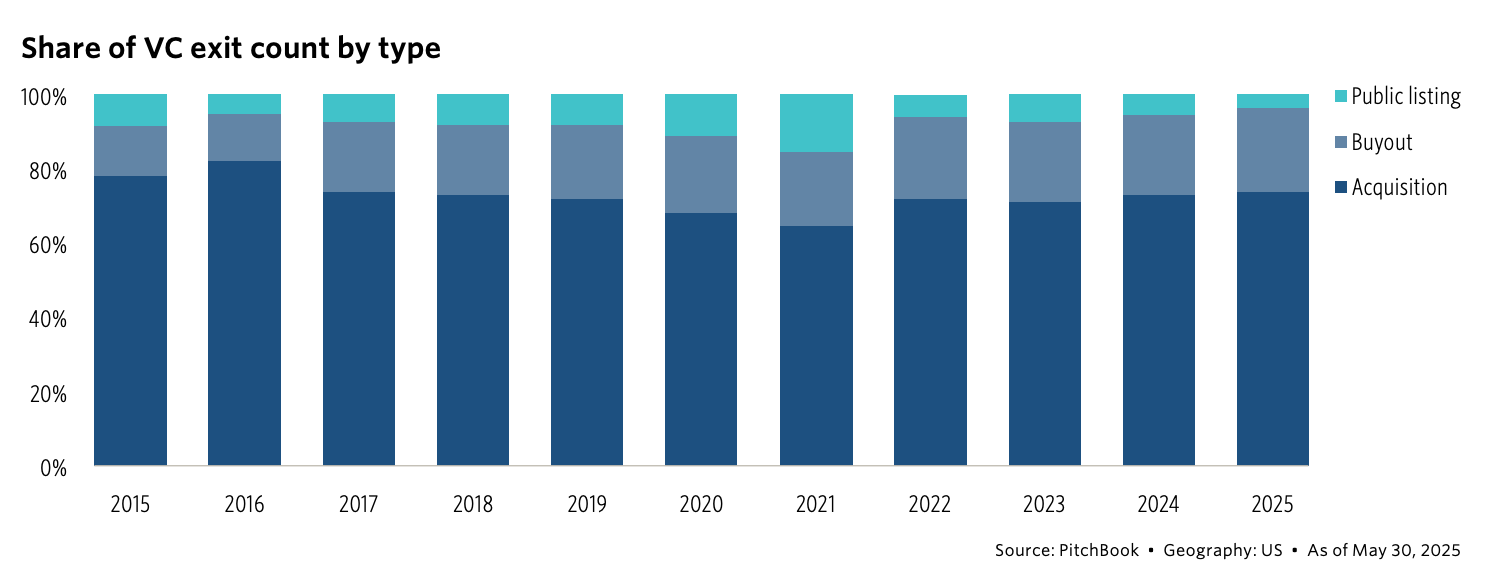

M&A Steps In—With Startups as Buyers

Acquisitions have become the primary exit route. As of midyear, M&A accounts for over 73% of VC-backed exits—

“the highest level since 2017.”

And it’s not just corporates buying:

“VC-backed companies have emerged as significant buyers,” with 36% of deals involving a VC-backed acquirer.

Cash-rich startups are consolidating where others pause. It’s a defensive and offensive play—shoring up growth while valuation pressure lingers.

Secondary Market Matures

With IPOs and M&A options limited, secondaries are filling the gap. PitchBook estimates the U.S. VC direct secondary market has reached ~$60B, up from $50B in 2024. The biggest shift?

“Average and median secondary pricing flipped to premiums in Q1 2025.”

That premium pricing reflects real appetite for exposure to top-tier companies. For LPs and GPs alike, secondaries have become a more viable liquidity tool—not just a fallback.

Fundraising Still Lags

Capital formation is tracking below expectations. PitchBook originally projected ~$90B in VC fundraising for 2025, but midyear data shows a slower pace—especially for first-time managers and sub-$100M funds.

“Continued fundraising pressure” is the key theme, though PitchBook notes potential upside in H2 if exits improve.

For now, GPs should assume longer timelines and more selective LP interest.

Final Take

PitchBook’s midyear update paints a market at a crossroads. AI and secondaries offer bright spots. But structural friction—from delayed exits to uneven capital availability—continues to define the cycle.

As the report summarizes:

“The second half of 2025 will test the sustainability of these emerging trends amid the ongoing liquidity crunch.”

Whether that crunch eases—or tightens—depends on how much more liquidity can be unlocked in the months ahead. For now, patience and creativity remain essential.

That’s all for today folks! Thanks for your support and spreading the word! Share this on Twitter or LinkedIn to help grow “the crew!”

Every Tuesday/[Thursday], we publish VC/CFO insights that matter - highlights from notable VC GPs, LPs, and CFOs/finance pros. Check out our VC Fund Playbooks, Models, Budgets, & Compliance Checklists @ AirstreamAlpha Products! Need more help? Check out Fund CFO Support provided by the Airstream Alpha

Love what we’re doing? Consider upgrading to paid for deeper dives on Thursdays (most paid subscribers expense these insights!). Top recent posts: