#234 What Just Happened in VC? A Look at Q1 2025 (NVCA Venture Monitor)

Another quarter down, and it’s safe to say U.S. venture is still finding its footing.

Q1 2025 wasn’t short on headlines—between massive AI mega-rounds and a sluggish fundraising climate, the vibe is... mixed. Some things feel eerily familiar (AI is still the darling), while others signal a shift (tariffs, cautious LPs, a venture debt tilt).

We went through the latest PitchBook-NVCA Venture Monitor (full report linked) so you don’t have to. Below are the themes that stood out to us as well as some great visuals that help us understand where the market is going.

Key Takeaways

VC Deal Activity Shows Concentration in Large Deals

The top 10 deals over $500 million accounted for 61.2% of total VC investment this quarter—OpenAI’s $40 billion round alone skewed that figure, and the other nine mega‑deals still made up 27% of all funding.

“The 10 transactions exceeding $500 million accounted for 61.2% of the total VC investment during the quarter.”

Cautious Investor Sentiment Amid Tariffs & Uncertainty

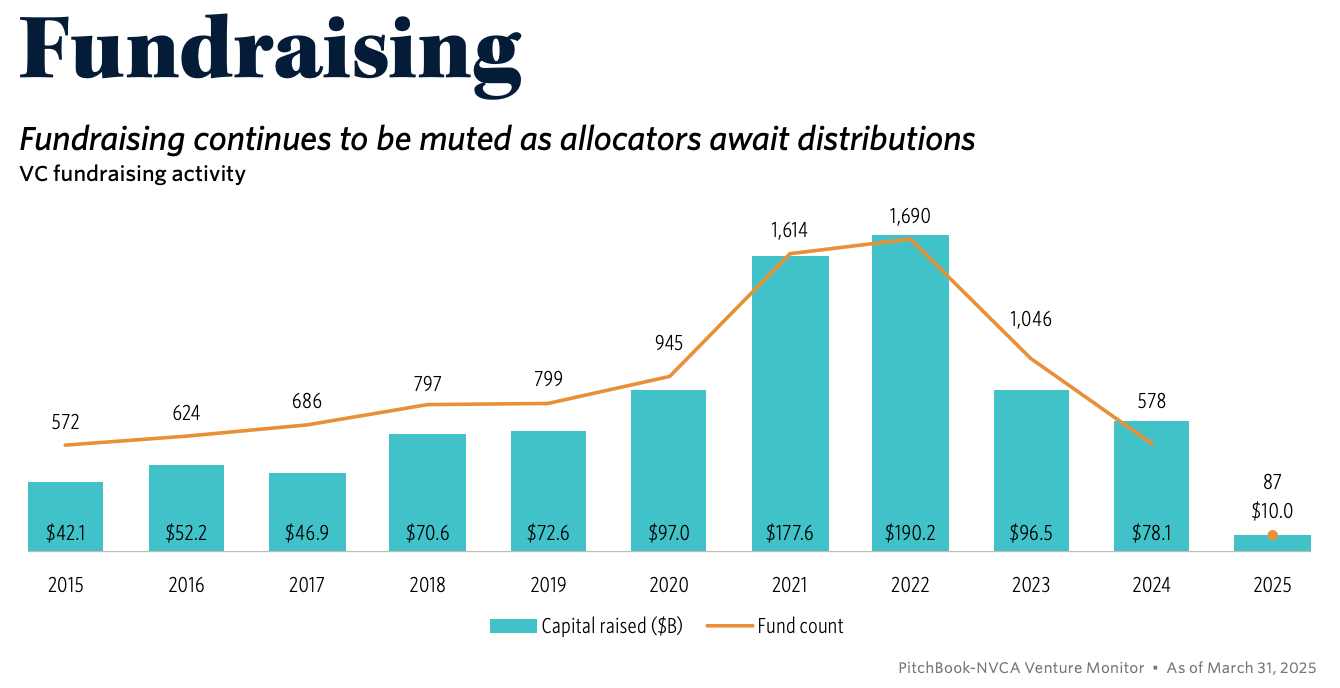

Ongoing tariff threats and market volatility drove fundraising to its lowest quarterly haul in a decade, with just $10 billion in new commitments. Investors are playing “wait‑and‑see.”

“Should the latest iteration of tariffs stand, we expect significant pressure on fundraising and dealmaking in the near term as investors sit on the sidelines and wait for signs of market stabilization.”

Exit Market Concentrated but Selectively Active

Exit value hit its highest since Q4 2021—thanks to Wiz’s blockbuster acquisition and CoreWeave’s IPO—yet only 12 companies went public. Notably, 76% of M&A deals closed before a Series B, signaling acquirers’ appetite for younger startups.

“76% of completed acquisitions in Q1 occurred before a Series B was raised.”

AI Startups Outpace the Pack

Despite the chill elsewhere, AI companies are thriving. The VC Dealmaking Indicator remains staunchly investor‑friendly for AI plays, buoyed by continued LP appetite.

“The VC Dealmaking Indicator remains staunchly investor‑friendly for AI companies.”

A Few Notable Trends

1. Corporate VCs Are Still Showing Up—for AI

CVCs are dialing back overall, but they’re showing real commitment to AI. In Q1, 41% of all CVC deals were AI-related—the highest share ever recorded.

This reflects a broader strategy shift: rather than acquiring AI startups outright, corporates are preferring to invest through VC. It lets them integrate innovation more gradually (and cheaply) into their existing stack. That said, some may pull back if tariffs start hitting cost structures.

“In Q1, corporate investors continued to play a significant role in VC, though their participation continues to decline as a share of total deals. CVCs have increasingly focused on AI companies, representing about 41% of all CVC deals in Q1—the highest share we have recorded.”

“The prospect of incorporating AI into business processes, products, and applications is not only encouraging AI adoption but also creating a compelling investment narrative for corporates, which appear to be favoring VC-based exposure over M&A strategies.”

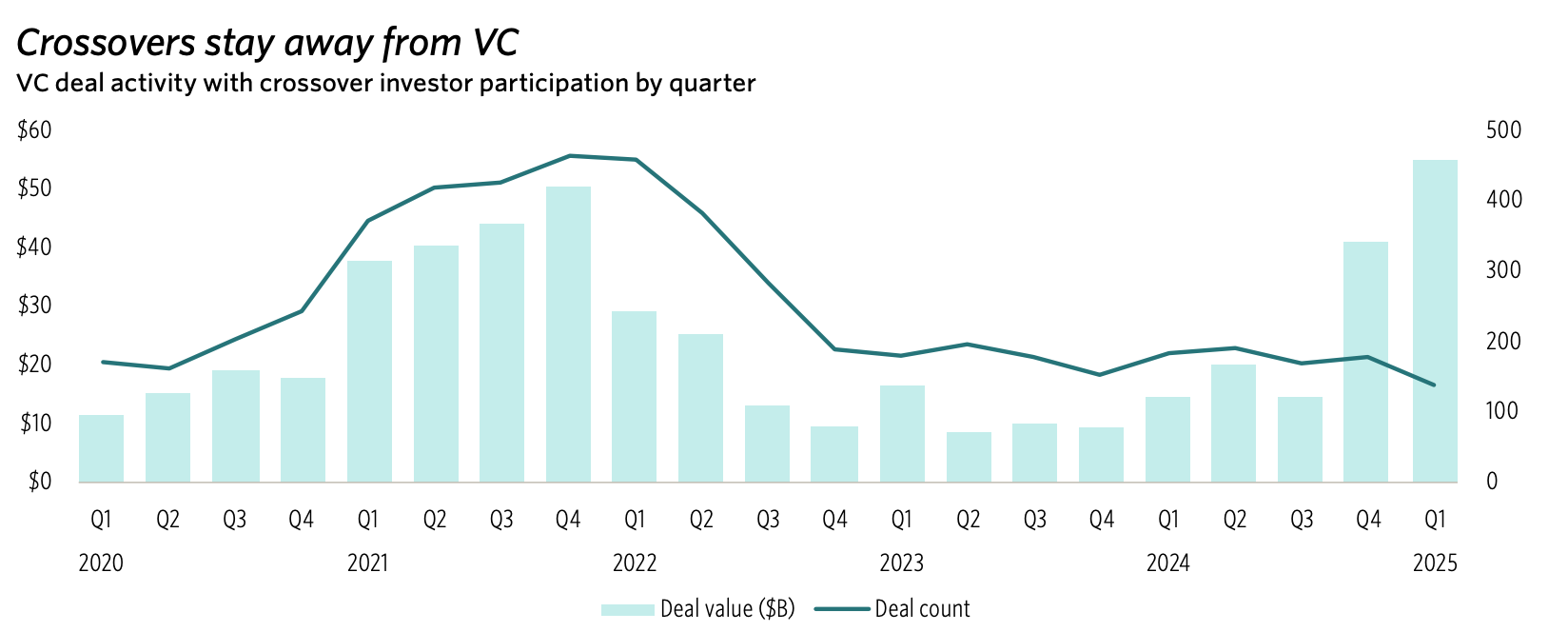

2. Crossover & Hedge Funds Are Still on the Sidelines

Remember the 2021 frenzy when hedge funds and crossover investors flooded into venture? That moment has clearly passed.

These players are still way off their previous levels—holding around 170 deals per quarter, which is about a third of their peak. The biggest issue? Lack of IPOs makes it hard to exit, so they’re staying on the sidelines until the public markets heat up again.

“Crossover firms have been largely unable to exit from significant positions built up several years ago, and this group is unlikely to get more involved in the market, absent a strong revival in IPOs.”

“Similarly, many hedge funds that added VC strategies during the boom years appear to have shifted away from the market in favor of more liquid asset classes.”

3. Private Equity Quietly Ramps Back Up

PE firms aren’t making headlines, but they’re gradually ramping their VC activity back up. Nothing explosive yet—but worth watching. This feels like a recalibration moment more than a full-scale return.

Venture Debt: Quiet Strength

While equity investors tread cautiously, venture debt kept humming along.

1. Strong Lending Momentum

Q1 saw about $11.6B in venture debt deals. Most of it went to tech (especially AI), while healthcare lagged behind.

2. Shift Toward Late-Stage Lending

Lenders are clearly leaning toward more mature startups. 83% of Q1 venture debt was deployed into later-stage companies. Early-stage debt is down sharply, which makes sense—lenders want more predictable revenue and less risk.

“Early-stage lending has swiftly declined, while venture growth accounts for 83% of Q1 lending.”

“Median and average late-stage venture debt deal values remain muted, but large deals are driving averages higher.”

Want to Go Deeper?

If you’re trying to make sense of what this all means for your fund, we’ve created several tools to help you analyze the current environment.

Our VC Toolkit (Premium)

We’ve put together practical templates and models to help funds better understand how changes in the market impact portfolio value, carry, and budgeting. If you’d like access to this template and other premium VC tools and models, feel free to reach out!

Keep reading with a 7-day free trial

Subscribe to @TheFundCFO Newsletter to keep reading this post and get 7 days of free access to the full post archives.