#225 TrueBridge State of VC Deep Dive

& What It Means for 2025+

👋 Hi, I’m Doug! Welcome to @TheFundCFO crew! Every Tuesday/[Thursday], we publish VC/CFO insights that matter - highlights from notable VC GPs, LPs, and CFOs/finance pros. Check out our VC Fund Playbooks, Models, Budgets, & Compliance Checklists @ AirstreamAlpha Products!

Need more help? Check out Fund CFO Support provided by the Airstream Alpha Team.

Love what we’re doing? Consider upgrading to paid for deeper dives on Thursdays (most paid subscribers expense these insights!).

Top Recent Posts - Check Them Out!

#219 Size Matters in VC (Cont'd) & DPI / Premium Carry Templates

#218 Size Matters: Small vs. Big VC (5x+ vs. 2x+), Lightspeed Returns Detail

Diving into the State of Venture Capital in 2025

Every year TrueBridge does a deep dive on the venture industry to identify key takeaways from the last year, highlight the most significant trends, and prepare for what is to come. Here is a link to their PDF: State of Venture Capital Industry.

Let’s take a deep dive in their analysis of the challenges 2024 presented and where we could be headed in 2025.

Key Takeaways

“The year will be a perfect storm, with venture capital, AI, crypto, politics, IPOs, and M&A all converging. -Ethan Kurzweil, General Partner at Chemistry”

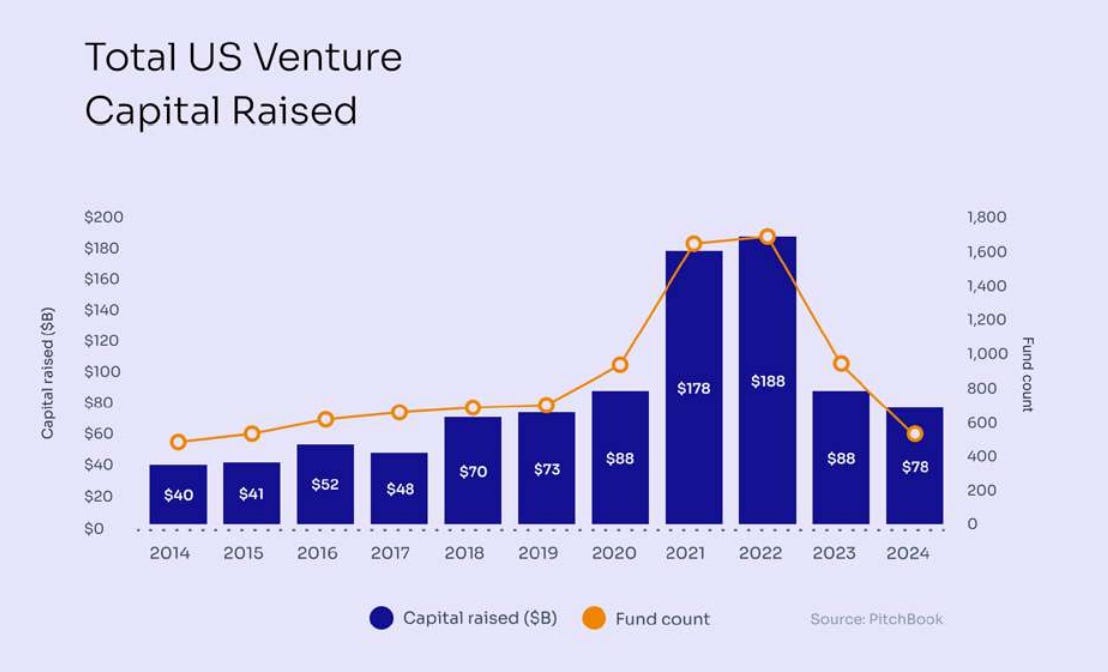

Fundraising: The Flight to Quality

Fundraising across the US venture ecosystem in 2024 reflected the market adjusting to tighter conditions.

Nearly $80 billion was raised across 508 funds, marking the lowest numbers recorded since 2019 and nearly 60% below the peak of 2022. Record-breaking commitments in prior years, paired with the limited liquidity of today’s market, has resulted in a more cautious venture environment. The shift to constraining capital has led LPs to prioritize established managers, concentrating capital among proven performers.

As established managers pulled away in fundraising rounds, emerging managers expectantly faced significant headwinds. Without the validation of strong exits, many struggled to raise follow-on funds, securing just 20% of total capital raised. First-time funds struggled the most to secure necessary capital, with fund counts and total capital raised falling to decade lows.

Investing: Early-stage activity drives optimism

The pace of dealmaking in 2024 remained measured compared to the oversubscribed frenzy of the pandemic years, yet encouraging signs of recovery began to emerge.

Deal count reached an estimated 15,260 transactions, marking the third-highest annual total since 2014 and a 29% increase over 2023 in capital invested. Venture-backed companies collectively raised $209 billion in 2024, surpassing prepandemic levels but remaining well below the highs of the zero-interestrate-policy (ZIRP) era.

In 2024, early-stage transactions saw notable growth, with a 17% increase in deal count and a 33% rise in deal value compared to 2023, reversing a two-year decline.

AI and machine learning solidified their position as dominant forces in 2024, capturing over 46% of all venture capital deployed during the year. AI investments were a major driver of deal activity across all stages, accounting for 77% of capital invested at the seed stage, and nearly half of the capital invested in Series D rounds and beyond.

Trend: The Great Institutionalization of VC Secondaries

Secondaries are quickly becoming a standard tool in venture capital for both managers and limited partners. Deal volume in the secondary VC market was estimated to be more than $100 billion in 2024. With that rise came a wave of headlines about eye-popping discounts, mega fundraises, and claims of the death of the IPO.

A key trend in 2024? Companies continued to stay private longer. The median age of companies raising Series D or later rounds hit a neardecade high of 9.7 years. Meanwhile, VC-backed exits were at historic lows, putting additional pressure on LPs. This combination of factors pushed many investors looking to unlock liquidity to the secondary market.

As companies delay their IPOs, secondary transactions provide early investors with a way to realize returns without waiting for traditional exits.

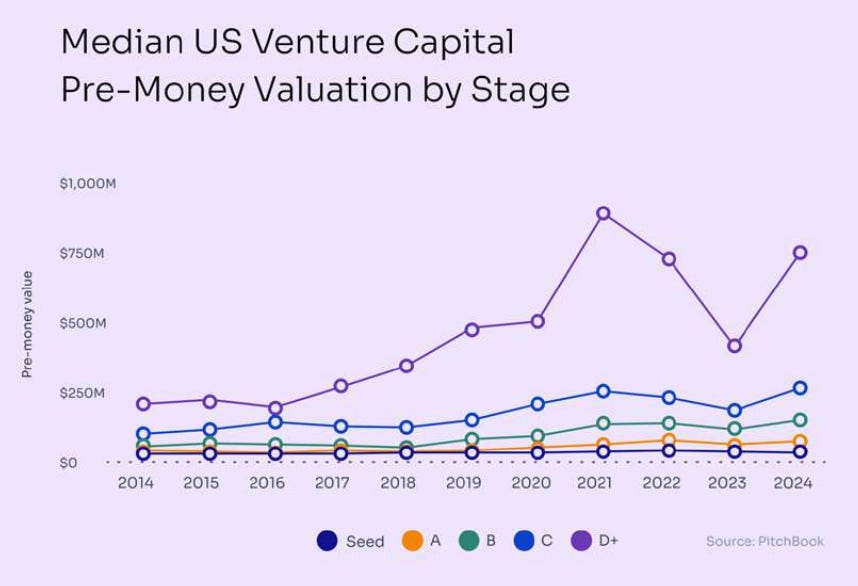

Valuations: The recovery and AI premium

Pre-money valuations across all stages increased in 2024. Median valuations at the seed and Series A stages each increased by approximately 25% and reached decade highs of $14 million and $40 million, respectively. While Series B valuations likewise increased year-over-year, the 42% and 112% increases at the Series C and Series D+ stages, respectively, were most notable, reflecting investors’ enthusiasm for standout companies with proven traction and growth, and opportunities with clear scaling potential.

With AI capturing nearly half of all venture capital deployed in 2024, it is clear that the narrative around valuations is increasingly tied to advancements in this space. Meanwhile, the extended time between first VC round and exit, averaging 8.5 years for unicorns, suggests that much of the ecosystem’s value remains locked up in private markets. Investor demand for AI-driven innovation is likely to persist and impact valuation trends, but valuations will also be impacted by the overall health of the financing and exit markets.

Blockchain Trend: Combating digital deception

Cyber deception has reached a new level of sophistication, and the rise of deepfake technology is making it harder to trust online content. From manipulating videos and audio to fabricating text, AI-generated forgeries pose serious risks to individuals, organizations, and industries. As the technology behind deepfakes improves, the threat of fraud and misinformation will only increase, making robust, immutable authentication systems more critical than ever. Blockchain offers a promising solution to this emerging crisis.

While blockchain presents a powerful tool against cyber deception, mass adoption remains a challenge. The success of blockchain-based solutions depends on large-scale buyin from platforms, media outlets, and consumers. In addition, these systems will need to adapt continuously as deepfake technology evolves.

Conclusion: Looking ahead with optimism

While the challenges have not disappeared, there are several reasons for optimism across the U.S. venture capital industry in 2025, building off some positive signals in 2024. At a high level, the regulatory environment is likely to ease due to the new US administration.

With a more permissive administration, combined with large cash reserves of key technology companies, we could see more and larger scale M&A transactions, resulting in much needed liquidity for the industry. And if a few promising venture-backed unicorn IPOs find positive market reception, the exit floodgates could finally open.

Link to Top Premium Content (Premium Subscribers)

Here’s a link to some of our top premium content related to DPI. If you want to dive deeper into fund modeling, DPI strategies, and other premium content tailored to venture capital and finance professionals, feel free to message me!

Keep reading with a 7-day free trial

Subscribe to @TheFundCFO Newsletter to keep reading this post and get 7 days of free access to the full post archives.